The point of initiation for any project is invariably a capital budget that outlines the project’s anticipated revenues and expenses. Monitoring these figures and comparing them to actual results can give a firm an accurate picture of its financial performance. Disparities between expected and actual figures may also prompt a revision of strategies or identification of areas needing improvement. Therefore, capital budgeting is an essential tool in the ongoing evaluation and enhancement of a company’s fiscal performance.

Overlooking opportunity cost implications

Capital budgeting process is a necessary and critical process for a company to choose between projects from a long-term perspective. Therefore, it is necessary to follow before investing in any long-term project or business. Luckily, this problem can easily be amended by implementing a discounted payback period model.

Payback Period Method

Finally, find the nth root of their ratio, subtract 1, and multiply by 100. ARR ignores the the time value of money, uses accounting profits instead of cash flows, and doesn’t consider the timing of returns. It may provide misleading results for projects with uneven profit patterns or different life spans. IRR can be misleading for projects with unconventional cash flows, potentially yielding multiple rates. It doesn’t consider project size or duration, assumes reinvestment at the same rate, and may conflict with NPV when comparing mutually exclusive projects. IRR provides a straightforward percentage return metric that’s easily comparable across investments.

Assess associated risks

Modern spreadsheet applications can automatically calculate IRR using built-in functions. Methods of capital budgeting enable businesses to distribute their financial resources efficiently across various investment opportunities. Therefore, we pick the next method to calculate the rate of return from the investments if done in each of the two projects. It now provides an insight that Project A would yield better returns (14.5%) than the 2nd project, which is generating good but lesser than Project A.

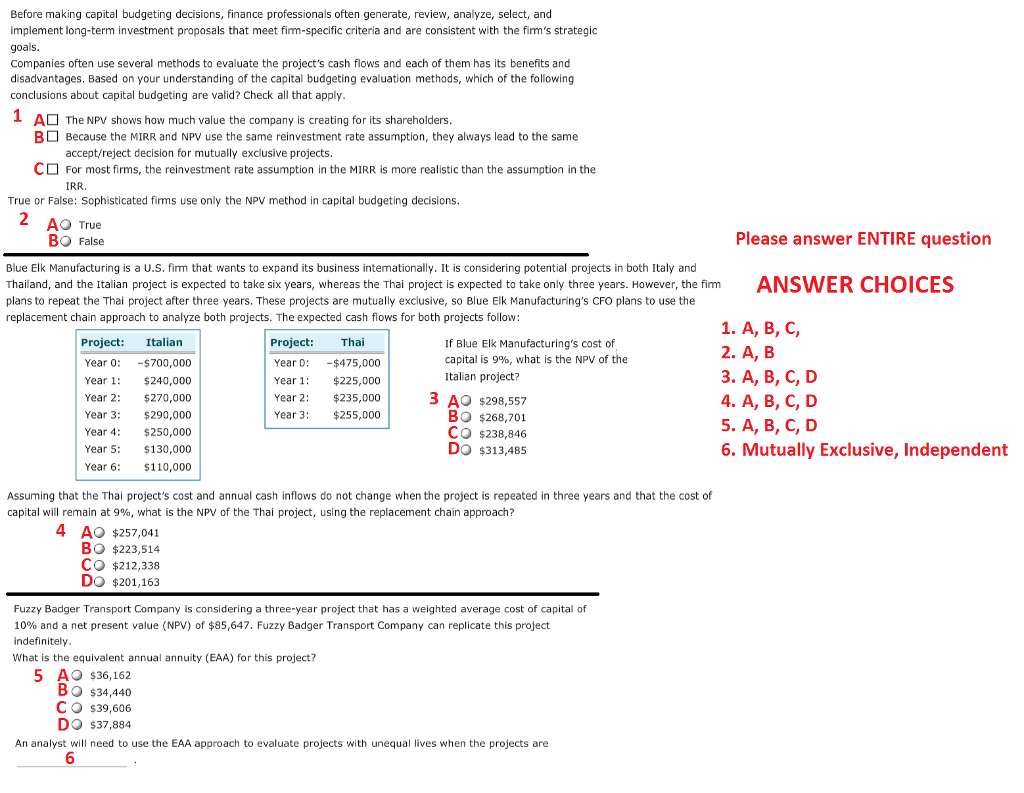

A capital budget is a long-term plan that outlines the financial demands of an investment, development, or major purchase. As opposed to an operational budget that tracks revenue and expenses, a capital budget must be prepared to analyze whether or not the long-term endeavor will be profitable. Capital budgets are often scrutinized using NPV, IRR, and payback periods to make sure the return meets management’s expectations. A dramatically different approach to capital budgeting is methods that involve throughput analysis. Throughput methods often analyze revenue and expenses across an entire organization, not just for specific projects. Throughput analysis through cost accounting can also be used for operational or noncapital budgeting.

Using capital budgeting along with the other types of managerial accounting will give you a competitive advantage. With this capital budgeting method, you’re trying to determine how long it’ll take for the capital budgeting project to recover the original investment. In other words, how long it’ll take for the major project to pay for itself. Yes, capital budgeting techniques are scalable and can be applied to projects of any size, though the complexity of analysis may vary based on project scope. Yes, regular evaluation is essential to track performance, adjust strategies based on changing market conditions, and ensure investments continue to align with organizational objectives. This reduction in errors leads to more reliable investment evaluations and better-informed decision-making, ultimately improving the quality of capital budgeting outcomes.

However, the payback method has some limitations, one of them being that it ignores the opportunity cost. Project managers can use the DCF model to decide which of several competing projects is likely to be more profitable and worth pursuing. However, project managers must also consider any risks involved in pursuing one project versus another. While unexpected events can disrupt short-term cash flow, the timeframes involved are shorter, allowing for quicker adjustments. Another noteworthy software solution is the Oracle Hyperion Planning tool.

- As such, our average return is biased upwards (as we will likely earn much less than the 29% needed on reinvested cash flows).

- This method is suitable in industries where mechanical and technical changes are routine.

- Both companies cater to a “middle market.” In October 2006, Kohl’s announced plans to open 65 new stores.

- Investments in heavy machinery or big constructions are examples of capital budgeting.

- A capital budgeting decision is both a financial commitment and an investment.

This heightened scrutiny leads to a more detailed analysis of potential returns, strategic importance, and long-term benefits. The concept helps businesses understand how much future returns are worth in today’s terms. Management preferences regarding project size, duration, risk level, and strategic alignment can impact project selection and evaluation criteria.

Automated systems significantly speed up the project evaluation process by quickly analyzing large amounts of data and performing complex calculations. Implement robust systems for monitoring actual project performance against initial projections. Consider best-case, worst-case, and most likely scenarios when evaluating projects. This collaborative approach key costs related to management and cost accounting improves decision quality and creates better buy-in for successful project execution. Their diverse perspectives help identify potential challenges, opportunities, and implementation considerations. Organizations should account for indirect costs like training, system integration, maintenance, and potential disruptions to existing operations.

Limited capital availability drives organizations to seek innovative financing options and alternative funding sources. Capital rationing emphasizes the importance of portfolio-level returns rather than individual project performance. Time value of money principles provide the basis for calculating key profitability metrics like NPV and IRR.